Sampling from complex probability distributions is important in many fields, including statistical modeling, machine learning, and physics. This involves generating representative data points from a target distribution to solve problems such as Bayesian inference, molecular simulations, and optimization in high-dimensional spaces. Unlike generative modeling, which uses pre-existing data samples, sampling requires algorithms to explore high-probability regions of the distribution without direct access to such samples. This task becomes more complex in high-dimensional spaces, where identifying and accurately estimating regions of interest demands efficient exploration strategies and substantial computational resources.

A major challenge in this domain arises from the need to sample from unnormalized densities, where the normalizing constant is often unattainable. With this constant, even evaluating the likelihood of a given point becomes easier. The issue worsens as the distribution’s dimensionality increases; the probability mass often concentrates in narrow regions, making traditional methods computationally expensive and inefficient. Current methods frequently need help to balance the trade-off between computational efficiency and sampling accuracy for high-dimensional problems with sharp, well-separated modes.

Two main approaches that tackle these challenges, but with limitations:

- Sequential Monte Carlo (SMC): SMC techniques work by gradually evolving particles from an initial, simple prior distribution toward a complex target distribution through a series of intermediate steps. These methods use tools like Markov Chain Monte Carlo (MCMC) to refine particle positions and resampling to focus on more likely regions. However, SMC methods can suffer from slow convergence due to their reliance on predefined transitions that could be more dynamically optimized for the target distribution.

- Diffusion-based Methods: Diffusion-based methods learn the dynamics of stochastic differential equations (SDEs) to transport samples before the target distribution. This adaptability allows them to overcome some limitations of SMC but often at the cost of instability during training and susceptibility to issues like mode collapse.

Researchers from the University of Cambridge, Zuse Institute Berlin, dida Datenschmiede GmbH, California Institute of Technology, and Karlsruhe Institute of Technology proposed a novel sampling method called Sequential Controlled Langevin Diffusion (SCLD). This method combines the robustness of SMC with the adaptability of diffusion-based samplers. The researchers framed both methods within a continuous-time paradigm, enabling a seamless integration of learned stochastic transitions with the resampling strategies of SMC. In this manner, the SCLD algorithm capitalizes on their strengths while addressing their weaknesses.

The SCLD algorithm introduces a continuous-time framework where particle trajectories are optimized using a combination of annealing and adaptive controls. From a prior distribution, particles are guided toward the target distribution along a sequence of annealed densities, incorporating resampling and MCMC refinements to maintain diversity and precision. The algorithm uses a log-variance loss function, ensuring numerical stability and effectively scales in high dimensions. The SCLD framework allows for end-to-end optimization, enabling the direct training of its components for improved performance and efficiency. Using stochastic transitions rather than deterministic ones further enhances the algorithm’s ability to explore complex distributions without falling into local optima.

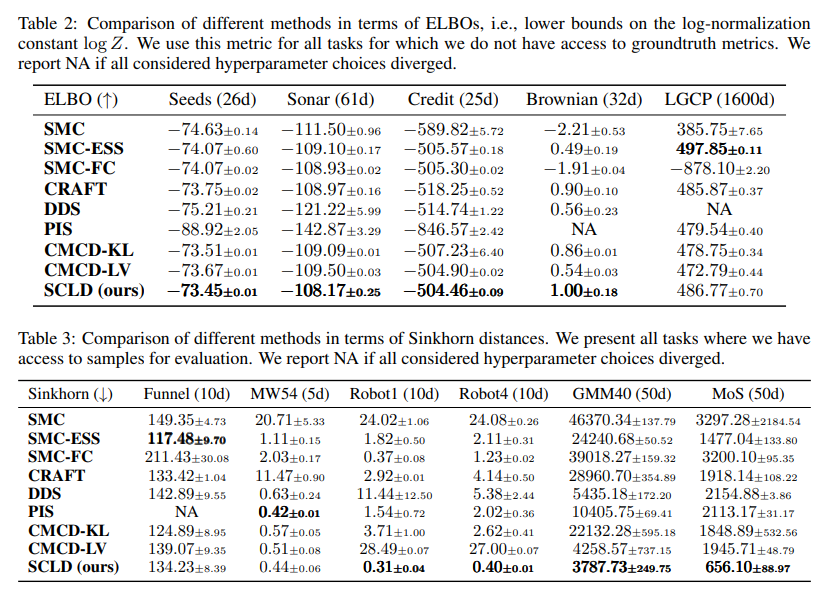

The researchers tested the SCLD algorithm on 11 benchmark tasks, encompassing a mix of synthetic and real-world examples. These included high-dimensional problems like Gaussian mixture models with 40 modes in 50 dimensions (GMM40), robotic arm configurations with multiple well-separated modes, and practical tasks such as Bayesian inference for credit datasets and Brownian motion. Across these diverse benchmarks, SCLD outperformed other methods, including traditional SMC, CRAFT, and Controlled Monte Carlo Diffusions (CMCD).

The SCLD algorithm achieved state-of-the-art results on many benchmark tasks with only 10% of the training budget other diffusion-based methods require. On ELBO estimation tasks, SCLD achieved top performance in all but one task, utilizing only 3000 gradient steps to surpass results obtained by CMCD-KL and CMCD-LV after 40,000 steps. In multimodal tasks like GMM40 and Robot4, SCLD avoided mode collapse and accurately sampled from all target modes, unlike CMCD-KL, which collapsed to fewer modes, and CRAFT, which struggled with sample diversity. Convergence analysis revealed that SCLD quickly outpaced competitors like CRAFT, with state-of-the-art results within five minutes and delivering a 10-fold reduction in training time and iterations compared to CMCD.

Several key takeaways and insights arise from this research:

- The hybrid approach combines the robustness of SMC’s resampling steps with the flexibility of learned diffusion transitions, offering a balanced and efficient sampling mechanism.

- By leveraging end-to-end optimization and the log-variance loss function, SCLD achieves high accuracy with minimal computational resources. It often requires only 10% of the training iterations needed by competing methods.

- The algorithm performs robustly in high-dimensional spaces, such as 50-dimensional tasks, where traditional methods struggle with mode collapse or convergence issues.

- The method shows promise across various applications, including robotics, Bayesian inference, and molecular simulations, demonstrating its versatility and practical relevance.

In conclusion, the SCLD algorithm effectively addresses the limitations of Sequential Monte Carlo and diffusion-based methods. By integrating robust resampling with adaptive stochastic transitions, SCLD achieves greater efficiency and accuracy with minimal computational resources while delivering superior performance across high-dimensional and multimodal tasks. It is applicable to applications ranging from robotics to Bayesian inference. SCLD is a new benchmark for sampling algorithms and complex statistical computations.

Check out the Paper. All credit for this research goes to the researchers of this project. Also, don’t forget to follow us on Twitter and join our Telegram Channel and LinkedIn Group. Don’t Forget to join our 60k+ ML SubReddit.

Trending: LG AI Research Releases EXAONE 3.5: Three Open-Source Bilingual Frontier AI-level Models Delivering Unmatched Instruction Following and Long Context Understanding for Global Leadership in Generative AI Excellence….

Trending: LG AI Research Releases EXAONE 3.5: Three Open-Source Bilingual Frontier AI-level Models Delivering Unmatched Instruction Following and Long Context Understanding for Global Leadership in Generative AI Excellence….The post This AI Paper Sets a New Benchmark in Sampling with the Sequential Controlled Langevin Diffusion Algorithm appeared first on MarkTechPost.