Generative models have emerged as great tools for synthesizing complex data and enabling sophisticated industry predictions. In recent years, their application has expanded beyond NLP and media generation to fields like finance, where the challenges of intricate data streams and real-time analysis demand innovative solutions. Generative foundation models thrive on three primary elements:

- A large volume of high-quality training data

- Effective tokenization of information

- Auto-regressive training methods

The financial sector, with its dynamic interactions and vast repositories of granular data, represents a prime area for these models’ transformative potential.

Among many challenges, one of the most persistent challenges in financial markets is managing the enormous volume of trade and order data, which often requires granular analysis to extract actionable insights. Financial markets produce structured datasets that reflect real-time participant interactions, such as order flows and price movements. However, traditional analytical tools often need help to simulate or predict complex market behaviors effectively. The lack of adaptability in these systems means they need help to accommodate volatile market conditions or detect anomalies that could signal systemic risks. This limitation hampers the ability of financial institutions to make timely and informed decisions, especially in scenarios involving rare or extreme events.

Existing financial prediction tools rely on algorithms tailored for specific tasks, requiring regular updates to reflect changing market conditions. These tools are often resource-intensive, with limited scalability and adaptability. While they can manage large datasets somewhat, their inability to model interactions between individual orders and broader market dynamics reduces their predictive accuracy. Also, traditional systems need help handling tasks such as forecasting stock price trajectories, detecting manipulative market behaviors, or modeling the impact of significant market events.

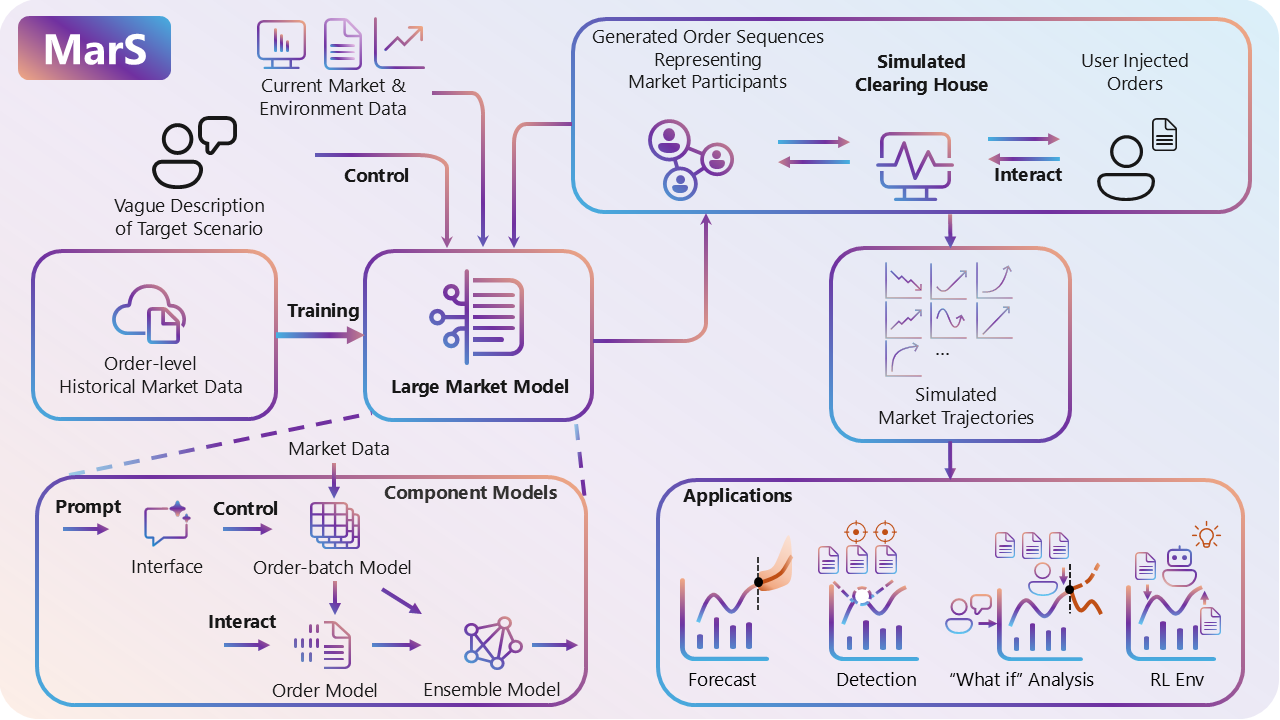

Microsoft researchers addressed these challenges by introducing a Large Market Model (LMM) and Financial Market Simulation Engine (MarS) designed to transform the financial sector. These tools, developed using generative foundation models and domain-specific datasets, enable financial researchers to simulate realistic market conditions with unprecedented precision. The MarS framework integrates generative AI principles to provide a flexible and customizable tool for diverse applications, including market prediction, risk assessment, and trading strategy optimization.

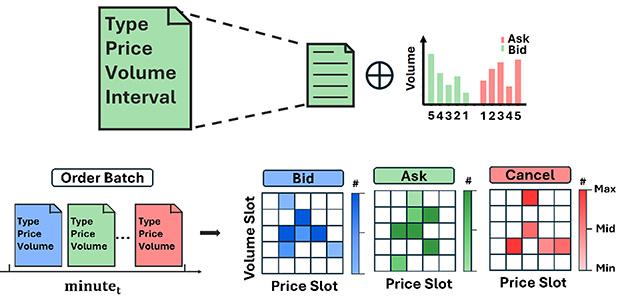

The MarS engine tokenizes order flow data, capturing fine-grained market feedback and macroscopic trading dynamics. This two-tiered approach allows the simulation of complex market behaviors, such as interactions between individual orders and collective market trends. The engine employs hierarchical diffusion models to simulate rare events like market crashes, providing financial analysts with tools to predict and manage such scenarios. Also, MarS enables the generation of synthetic market data from natural language descriptions, expanding its utility in modeling diverse financial conditions.

In rigorous tests, MarS outperformed traditional models in several key metrics. For example, MarS demonstrated a 13.5% improvement in predictive accuracy in forecasting stock price movements over existing benchmarks like DeepLOB at a one-minute horizon. This advantage widened to 22.4% at a five-minute horizon, highlighting the model’s effectiveness in handling longer-term predictions. MarS also proved instrumental in detecting systemic risks and market manipulation incidents. By comparing real and simulated market data, regulators could identify deviations indicative of unusual activities, such as differences in spread distributions during confirmed market manipulations.

Key takeaways from this research include:

- MarS demonstrated up to a 22.4% improvement in long-term predictions compared to traditional benchmarks.

- The engine supports various applications, from market trajectory simulations to anomaly detection.

- MarS incorporates real-time feedback, making it highly adaptable to dynamic market conditions.

- The hierarchical diffusion model enables high-fidelity modeling of rare financial scenarios like crashes.

- MarS provides a robust tool for regulators to detect systemic risks and monitor market integrity effectively.

- It provides an advanced reinforcement learning algorithms environment, ensuring robust real-world applications.

In conclusion, the research contributes to financial modeling by addressing the critical limitations of traditional tools. MarS and LMM performed exceptionally in processing vast order flow datasets. Specifically, MarS improved predictive accuracy by 13.5% at a one-minute horizon and 22.4% at a five-minute horizon compared to benchmarks like DeepLOB. Also, its capability to simulate market trajectories enabled precise anomaly detection, as seen in its analysis of spread distributions during manipulation events. By modeling rare scenarios such as market crashes using hierarchical diffusion methods, MarS ensures adaptability across diverse financial tasks.

Check out the Details and GitHub Page. All credit for this research goes to the researchers of this project. Also, don’t forget to follow us on Twitter and join our Telegram Channel and LinkedIn Group. If you like our work, you will love our newsletter.. Don’t Forget to join our 60k+ ML SubReddit.

[Must Attend Webinar]: ‘Transform proofs-of-concept into production-ready AI applications and agents’ (Promoted)

[Must Attend Webinar]: ‘Transform proofs-of-concept into production-ready AI applications and agents’ (Promoted)

The post Microsoft Research Introduces MarS: A Cutting-Edge Financial Market Simulation Engine Powered by the Large Market Model (LMM) appeared first on MarkTechPost.